RBI / MPC kept all rates unchanged as expected. The surprise here was rather external MPC member Prof. Varma voting for a 25 bps rate cut. Market was more looking forward to any dilution in the stance of policy, given the context of softer than expected recent CPI prints and government’s commitment to significant fiscal consolidation in the recent budget. In the event, the Governor didn’t yield much on the stance, which was retained as ‘focused on withdrawal of accommodation’. As expected, Prof. Varma dissented. As not expected, Dr. Goyal didn’t.

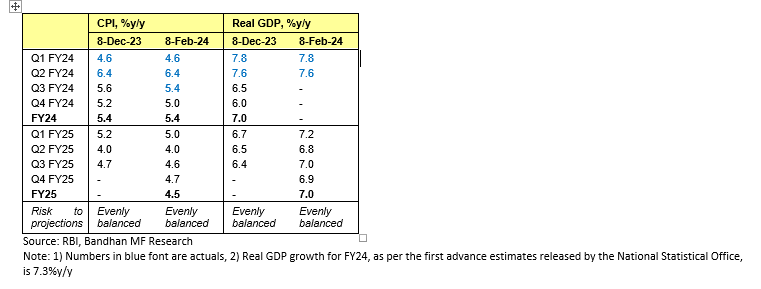

RBI’s forecasts were largely in line, and are summarized below:

The general assessment on growth is that of continued resilience backed by the momentum in investment demand, optimistic business sentiments and rising consumer confidence. This is also reflected in the GDP forecast for FY 25. On inflation, the progress on core inflation is noted and welcomed but so is the repeated occurrence of food shocks that is interrupting the pace of disinflation. Further supply side risks come from international geopolitical uncertainties.

Assessment

The underlying template for now seems similar for RBI and the Fed: strong growth is allowing for monetary policy to be patient in seeing through the attainment of respective inflation targets. More specifically, and focusing on the Indian context now, with price volatility driven by supply side factors resurfacing from time to time in context of robust underlying growth, there is always a chance of inflation pressures generalising. Put another way, the central bank has the luxury to not try and take a forward looking call (e.g. try to anticipate the effect on aggregate demand going ahead from fiscal compression shown in the just concluded interim budget) since concurrent growth if anything is stronger than what was earlier forecasted and doesn’t need any support for now from monetary policy.

RBI’s liquidity approach has evolved since late last year. Thus while the entire rate hike cycle was conducted in an environment of abundantly surplus liquidity, since late last year the central bank had started to worry about the quantum of excess system liquidity as well. This was presumably to facilitate greater transmission from banks. In the most recent period, however, RBI has become more responsive to anchoring overnight rate towards repo. While the Governor has noted that core liquidity remains positive, this is expected to progressively deteriorate into the financial year end predominantly on account of seasonal rise in currency in circulation. This, alongside ongoing large fluctuations in government cash balance, may require continued active intervention to anchor overnight rates. In all likelihood, overnight rates will range between repo and MSF over the next month and a half; with zero tolerance from RBI for it falling below repo rate. Alongside continued pressure of issuances, this should keep corporate bond spreads elevated over this period.

With respect to the conditions accompanying the current monetary policy stance (incomplete transmission and inflation above 4%), these are valid only so long as growth momentum holds. If that changes, then the current projection on inflation will be sufficient for both a stance change as well as follow up rate cuts, in our view. Projected real policy rate considerations are immaterial today given the strong growth momentum, but won’t be if this starts to change. To clarify, we aren’t arguing for any significant drawdown in growth trajectory. It is well understood that India’s structural growth drivers are strong. However, global cyclicality, fiscal compression, and the lagged impact of rate hikes are all reasons to expect some momentum slowdown in the year ahead. This, alongside the start of rate cuts in US and Europe around mid-year, should be enough to give more weight to voices within the MPC that are also closely tracking the evolution of real policy rates. Presumably Prof. Varma’s is one such voice, although we agree with the majority MPC that it is somewhat premature to be already actively contemplating rate cuts.

Takeaways

We were open to the idea of some soft indications of an impending shift in the liquidity stance, if only to determine whether RBI’s response to overnight fluctuations around the repo rate will be symmetrical or not. In the post policy press conference, Deputy Governor Patra did assert (later reiterated by Governor Das) that the objective is to keep weighted average overnight rate at repo rate. However, we would await further action here to be confident that this will indeed be the case, especially with anticipated declining core liquidity. That said, there isn’t much in the form of additional takeaways from the policy in our view. It is appropriate to continue to focus on inflation so long as growth momentum is this strong. However, the guidance today may not be a line in stone and considerations like real policy rate may gain more weightage as growth momentum slows.

Our bullish view on bonds isn’t predicated on an early or deep rate cut cycle (https://bandhanmutual.com/article/15865), but rather on the ongoing transformation in India’s underlying macro economic dynamics in context of greater foreign participation given impending bond index inclusion. This has potential to cut risk premia on bonds which most likely will be seen in continued compression in term premia. Thus bond performance is not as constrained by the extent of rate cuts as it would be if the starting point was flatter term premia (overnight rate to duration bond yield) and if one was only playing duration for cycle reasons. In fact, the view that one needs to be less tactical and more structural is even stronger post the budget where we, along with everyone else, have been very pleasantly surprised with the extent of fiscal consolidation the Finance Minister has put on the table.

We continue with overweight 30 year government bonds in our active duration and gilt funds. More broadly, we reiterate that focus of investors should be on appropriate duration enhancement as per risk appetite and a greater focus on quality bonds, unlike the focus on minimizing duration and maximizing carry that has been the dominant theme over the past couple of years.

Source: Bandhan MF Research

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of Bandhan Mutual Fund (formerly known as IDFC Mutual Fund). The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither Bandhan Mutual Fund (formerly known as IDFC Mutual Fund)/ Bandhan Mutual Fund Trustee Limited (formerly IDFC AMC Trustee Company Limited) / Bandhan AMC Limited (formerly IDFC Asset Management Company Limited), its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.