In response to a vicious second wave of the pandemic, the RBI governor has recently renewed his battle-cry and reinstated a ‘whatever it takes’ stance. As discussed in our note then (https://idfcmf.com/article/4583) this represents a shift from the more recent dovish but ‘steady as she goes’ approach and is somewhat more noticeable now given the multi-speed global re-emergence from the pandemic and the risks from imported tightening that it brings. Apart from a somewhat modified approach to guarding against external volatility which emphasizes more the accumulation of a forex reserve war-chest, our sympathy with the RBI also lies in our sense that the total public policy response in India so far to the pandemic has been somewhat more nuanced and restrained when compared with many other geographies around the world. This provides for some degrees of freedom in conducting policy this year, though these have to be still administered with due discipline. Given this context, we thought it an opportune time to reassess the RBI’s response thus far through looking at the evolution of its own balance sheet over the duration of the pandemic.

Source: RBI Weekly Statistical Supplements, IDFC MF Research

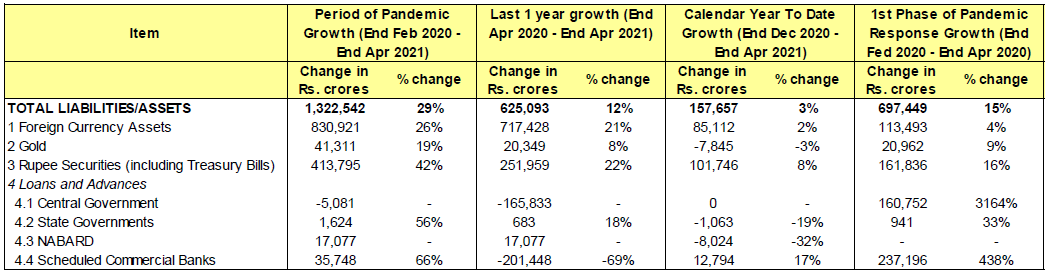

The table above presents key entries in the asset side of RBI’s balance sheet. The figures in the columns represent the growth in these entries for the period specified (in INR crores). The accompanying percentages changes are absolute (and not annualized) over the same period. For the purpose of this analysis, we divide the pandemic phase into the following (somewhat approximate) phases:

1. The First Phase: We have started the analysis as at end February 2020 and assumed the first phase response till end of April 2020. As can be seen in the last columns of the table, the RBI’s response was justifiably very aggressive during this period. Thus over a short span of 2 months, its balance sheet grew by 15%. The largest contributors to this growth were a sharp rise in loans to banks largely via the long term repo and targeted long term repo operations (LTRO and TLTRO) and a jump in financing to government. Alongside RBI also stepped up intervention to buy government bonds. Forex reserve accretion played a part but to a lesser degree than these 3 other operations.

2. The Next One Year: Over the one year that has now passed since the first emergency response described above, RBI’s balance sheet growth reverted to a more normal 12%. Importantly, it also reverted to a more conventional construction. Thus most if not all of the loans to the banks and to the government have been retired. The bulk of the balance sheet expansion has in fact happened via accretion of forex assets which has been an integral strategy in shoring up defenses for the country as discussed above. Indeed, this expansion is a source of great comfort at this juncture. Government bond (including treasury bill) holdings have been the second biggest contributor to the growth in balance sheet but the size of this expansion has been a much more sedate just over INR 2.5 lakh crores for the full year (versus over INR 1.6 lakh crores bought in just 2 months in the first phase response) and represents only 35% of the expansion that has been achieved via growth in forex assets over this period.

3. Calendar Year So Far: An additional data cut of interest is the growth in RBI’s balance sheet since the start of the calendar year 2021 (till end of April). This is of relevance especially since forex reserve growth peaked sometime towards end of January. As can be seen, not only has balance sheet growth slowed down but the peak contributor now has been expansion in government bond and treasury bill holdings rather than forex assets.

Summary and Conclusions

As can be seen from the above analysis, while RBI went aggressive and unconventional in the first phase response to the crisis, it soon reverted to a more conservative expansion and largely via the best of ways (expansion in forex reserves). Interventions in the bond market have continued, and the mode of such interventions have increasingly become more unconventional and indeed only a step removed from direct monetization. However, the total expansion in bond holdings over the past year has again not been noticeably excessive. As forex accretion has slowed this year, the pace of balance sheet expansion has further moderated (even on annualized basis) and pole position is now with government bond and treasury bill purchases. This leads us to the following 2 conclusions: One, and within bounds of reason, the relatively nuanced response so far (especially when combined with the total fiscal response) probably allows RBI to have somewhat larger operating space than what could otherwise have been the case. The recent statement and accompanying commitments from the governor can be thus looked at from this perspective. Two, if owing to the differential global recovery as well as a less robust private sector FDI pipeline, forex inflows were to be relatively slower this year then RBI can indeed play a larger role in supporting the government bond market. Thus the INR 3 lakh crore indicative commitment made by the governor earlier (and partly formalized via the G-SAP program) should be looked at as more of a ‘place-holder’ rather than the full extent of commitment from the central bank. It is also to be noted, and also within reason, that the appropriate response to evolving growth – inflation mix will be first via changing the price of overnight money and may still allow the inferences presented here to hold for the time being.

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.